How regularly should payroll professionals re-assess their choice of default fund?

At least once a year.

Super funds, like the businesses you all work for, are set up to provide an annual report and statement to each of their members just after the close of their financial year. For most super funds, this means 30 June. This is the ideal time to check how your super fund is going. When we do our annual fund performance reviews, we benchmark funds on their annual financial year outcomes for this reason.

Are there any types of fees that we should be wary of?

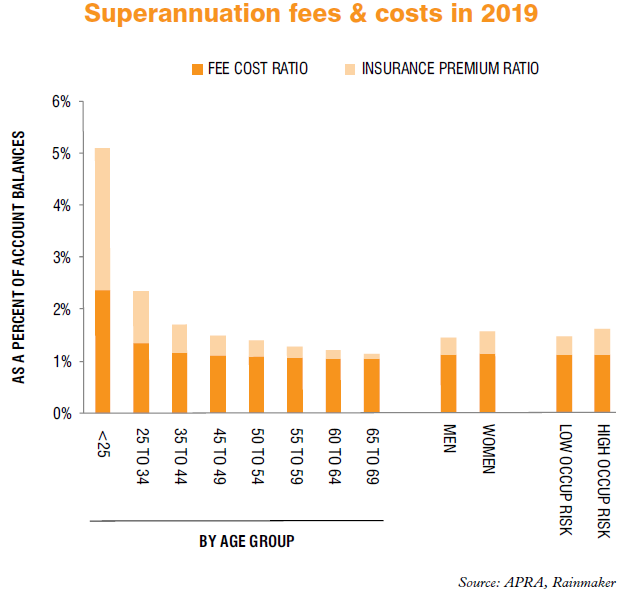

We used to tell super fund members to be wary of entry and exit fees. But very few funds charge entry fees nowadays. Exit fees, thanks to new laws just passed by the Parliament, are now banned. But there are still some fees that can be a bit tricky, for example, insurance administration charges or special compliance levies. While these fees are legitimate and allowable, the key message is that with superannuation the enemy is complexity.

This is why SelectingSuper believes super funds should be easy to understand, have clear descriptions of how they operate, and it should simply explain the fees they charge you.

Nevertheless, with increasing competition, most superfunds are working hard to lower their fees as much as they can. As a result the acid test question for fees is 'how much do they total to?' With fees now averaging around 1%, anything too much above that, say above 1.2%, is high price. But lots of super funds now charge fees that are much lower, some as low just 0.6%. Funds are even telling Rainmaker and SelectingSuper that they expect their fees in coming years to get even lower.

Super funds want your business and will compete hard to win it. Most will give companies corporate discounts on insurance premiums or a rebate on fees, though this depends on the type of fund, how high its baseline fees are and how big the company superannuation account is.

Is it appropriate to expect that the super funds that are attracting the most in-flows or which have the highest funds under management should generate the highest returns?

No. Super funds that get the most contributions or which are the biggest are most often the ones listed on the most Enterprise Bargaining Agreements, industrial awards or have the biggest sales distribution networks. While some of these popular funds are very good, not all are. Always judge your super fund on its merits.

Is a not for profit super fund better than retail super fund?

No. They are just different. Complicating this even further is that there is actually no formal legal definition of what 'not for profit' means in superannuation. Another twist is that some not for profit funds now like to be called 'profit for member' funds.

Rainmaker and SelectingSuper pays a lot of attention to whether a fund is not for profit or retail because it tells us much about that fund's history, where it came from, and how it is structured. For example, not for profit funds are usually run by boards of equal representative trustee directors, are usually simpler super funds and are often direct funds meaning you can join them without having to go through an intermediary like a financial or corporate adviser.

Sure, some not for profit super funds are very good funds that regularly achieve high returns while charging you low fees, but not all are. Some not for profit funds get surprisingly low returns. Conversely, some retail bank-owned super funds are today among the lowest cost super funds in Australia.

What is concerning is when a not for profit fund, especially a low performing one, markets itself as being a good fund only because it is not for profit. A good fund is a good fund irrespective its corporate structure.

Another way to look at this is that your company seeks to make a profit. That does not make it a bad company. The same applies to super funds. Judge your super fund on how well you trust it, does it achieve above average investment returns, does it charge fees that are fair, does it have sharply priced insurance, is it easy to deal with? If it does all these things, then it is a good fund.

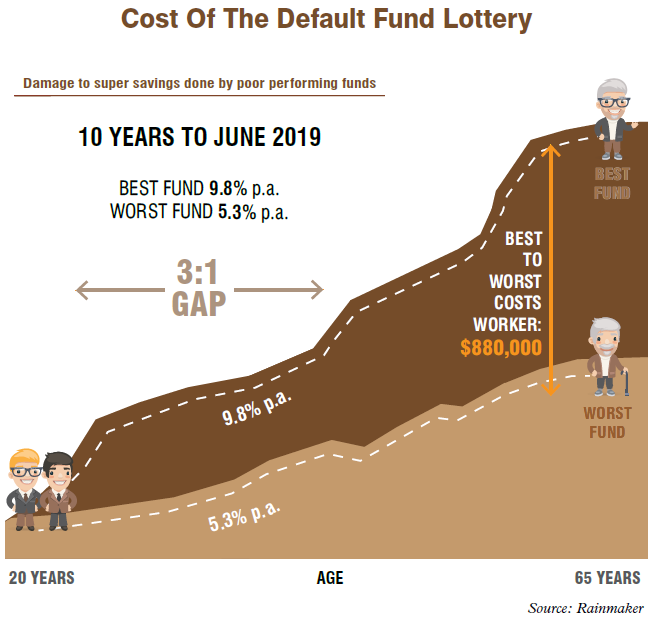

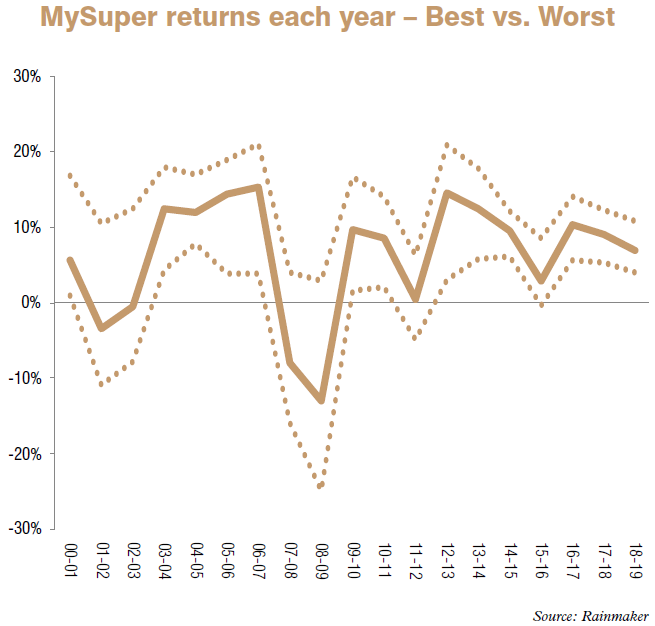

What is a good investment return?

Investment returns vary year by year depending on market conditions. What is a good return this year may not be so good next year. To help you make sense of this, super funds publish their investment return targets so you can get a sense of what they are aiming for.

For example, most MySuper products used by employers aim to beat inflation over the long run by 3 or 4% pa. With inflation being now slightly less than 2% p.a. this means they are aiming to achieve long run investment returns of 5% p.a. or more.

Most super funds don't just match their investment target, they beat it and sometimes by a wide margin. So even if a super fund beats its target we still end up looking for which are the top performing super funds. Viewed another way, a super fund may have a low declared investment target that is easy to beat. Just because it ends up achieving this goal doesn't make it a good fund.

Remember that the job of your super fund is to always be doing the very best they can to put as much extra money in our superannuation accounts as possible. While we want our super funds to achieve their targets, we also want to get the best returns they can.

Can payroll staff do more to encourage consolidation of superannuation for our staff? This might not be in the job description but may go a long way to retaining staff.

Yes they can. But payroll staff should put the priority for this in perspective. If helping your company's employees consolidate their superannuation accounts enables the company to streamline how it administers its superannuation, it could have direct benefits to the company. Most super fund members however contribute to just one super fund at a time so while consolidating superannuation accounts may be a good thing, it may not impact the company too much.

Just be careful that you avoid giving your employees de facto financial advice about which funds to consolidate into. For example, if they ask you if they should consolidate into the company's MySuper default and you implicitly say yes, that could be seen as you giving them advice. There might also be choice of fund implications if they wish to consolidate out of the company's default to their other preferred fund.

A better way to handle this would be tell them that consolidating super fund accounts is easy and that all an employee needs do is go to the fund's website and follow a few links. Indeed if it's hard to do then this might be a sign the fund is hard to work with and it might be time to switch to a smarter more organised fund.

Whatever you or your employees end up doing on this front, the bottom line is that consolidating super accounts is free. Be very wary of anyone or any service that tries to charge a fee or a commission for doing this.

How important is the insurance offering when selecting which default fund to choose?

The audience survey that SelectingSuper ran during the conference presentation revealed that most payroll staff believe fees are the most important thing to consider when choosing a super fund. Insurance premiums may not be what we normally mean by fees but for some members, particularly younger ones, these insurance premiums actually cost more than their regular super fund fees.

For example, for members aged in their twenties their standard cover insurance costs on average about $220 p.a., while for members aged in their fifties it costs on average about $600 p.a. If they've topped up their insurance it could be costing much more still.

So insurance should definitely be considered when you are deciding which super fund to join or whether you should switch funds. Rather than just look at the cost of the insurance you should also look at the value it represents, that is, the cost of insurance compared to the amount of cover provided. You should also look at whether the insurance cover matches the needs of your company's employees.

These comparisons may sound complex but there are ways to do this. Contact us if you want to know more, we'd be delighted to show how easy it can be to make sense of all this.

Are there any real benefits in going with an SMSF over an established fund?

Yes and no. It depends on the financial circumstances of the particular employee. But be careful, if company employees are asking their payroll teams these types of questions you are beginning to sail close to the edge of where financial advice begins. Rainmaker and SelectingSuper's view on this is that it's best to avoid discussing these details but instead refer to where they can get more information.

This is why The Good Super Guide and SelectingSuper website has information on this topic. Payroll staff who are asked about SMSFs are invited to refer company employees to check it out. Following this, you could suggest they contact their super fund and arrange to speak with one of their financial advisers, or suggest they speak to their own financial adviser or accountant.