Media Centre

< Back to Media Centre Home

SelectingSuper Media Release - Monday 10 April 2017

| |

| SUPERANNUATION PERFORMANCE - FEBRUARY 2017

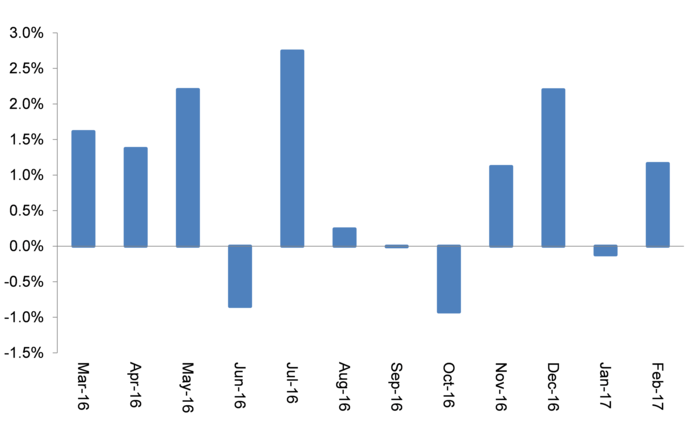

The SelectingSuper workplace default option MySuper Index increased by 1.2% in the month of February. The positive result in the month was underpinned by strong monthly returns in equities and property.

|

| |

| SelectingSuper MySuper Index - Monthly Returns |

|

![]()

|

| |

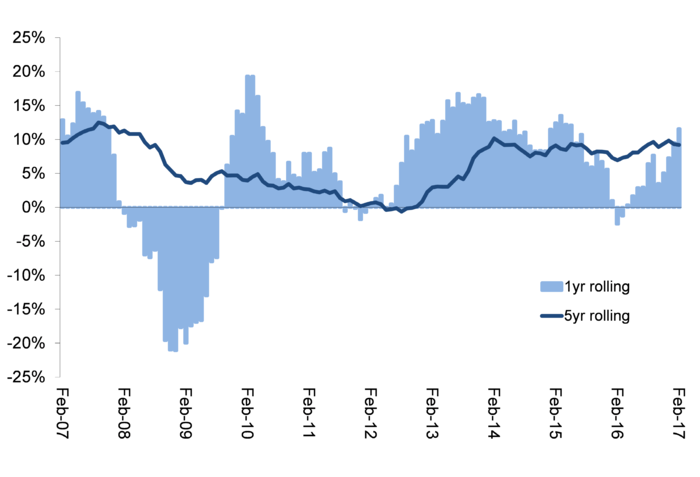

| The monthly rise brings the 12 month annual return to February 2017 to a very strong 11.6%. The top performing default fund returned 19% for the year ending February. Further highlighting this strength, over 75% of workplace default options achieved annual returns over 10%, and over 40% achieved annual returns over 12%.

February was the 11th straight month of positive average annual returns for the default segment after briefly slipping into negative in early 2016.

The performance over multi-year time periods continues to benefit from positive impact of the high returns since 2012. Reflecting this, three year rolling MySuper returns are 6.9% pa and five year returns are 9.2% pa. The longer term 10 year return is a more modest 4.7% pa, although this period incorporates the full effect of the GFC and is overlaid by a lower inflation environment.

|

| |

| SelectingSuper MySuper Index - Long Term Returns |

|

![]()

|

| |

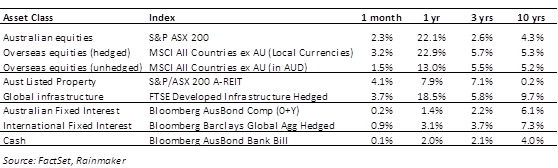

| On an annual basis Australian equities, often the largest asset class in many balanced funds, contributed with a very solid 22.1% return. Similarly the contribution of hedged international equities was 22.9% for the 12 months to February. The strengthening of the Australian dollar over the year resulted in a lower 13.0% return for unhedged international equities.

The infrastructure index continues to reflect strong returns in that segment over the short term, and even exceeding equities over the medium term. Property, which has provided a significant positive impact on investment outcomes over recent periods, dropped back to a more modest but solid contribution of 7.9%.

The movement in the yield curve in recent months has resulted in fixed interest returns dropping back both domestically and internationally, but still stablised to return positively to most portfolios.

In net terms this means growth orientated default options with relatively high exposure to equities, and infrastructure significantly outperformed in the 12 months to end February. Similarly funds with relatively larger holdings in fixed interest in the period underperformed.

|

| |

| Financial Market returns to February 2017 |

| |

|

![]()

|

| |

| Leading products: One year returns |

| The top 5 performing products in Workplace, Personal and Retirement markets over the 12 months to February 2017 are as follows: |

| |

| WORKPLACE SUPER (MYSUPER/DEFAULT) |

|

| CFS FirstChoice Lifestafe (1970-1974) |

19.0% |

| RBF Investment Account - MyPath 1970-1974 |

16.5% |

| LGS Accumulation Scheme - High Growth |

15.5% |

| Lutheran Super - Balanced |

14.8% |

| SA State Lump Sum Scheme - Growth |

14.2% |

| |

|

|

| IOOF Employer Super Personal - Profile 75 |

16.9% |

| FirstChoice Personal - FirstChoice Multi-Index Balanced |

14.8% |

| Rio Tinto Staff Super Personal - Growth |

13.7% |

| Mercer PS - Non Mercer Balanced Value Style |

13.1% |

| Catholic Super Personal - Balanced |

13.1% |

| |

|

|

| RBP Account Based Pension - Growth |

17.8% |

| IOOF ESP - Profile 75 |

16.5% |

| Lutheran Super Pension - Balanced |

16.4% |

| FirstChoice Pension - FirstChoice Multi-Index Balanced |

16.3% |

| MyLife Mypension - Moderately Aggressive |

15.8% |

|

| |

| Segment Performance |

|

Regarding the market segments, the gap between not-for-profit (NFP) funds and Retail funds within the Workplace sector continues. The 12 month return gap has, however, contracted to 50 basis points in favour of NFP funds. This decreases reflects the relatively higher performance of Retail funds in February underpinned by strong returns in listed equity markets.

The long term 5 year segment gap is 140 basis points in favour of NFP funds.

|