< Back to Media Centre Home

SelectingSuper Media Release - Friday 6 July 2018

SUPER FUNDS ARE AUSTRALIA'S BIGGEST INSURER

Superannuation funds are the biggest supplier of life insurance in Australia, providing insurance to 11 million account holders. Through these wholesale life insurance policies that super funds negotiate directly with their insurer, fund members are able to get life insurance cover at premium prices usually much cheaper than what they would have to pay if they bought the insurance themselves.

The average price of this life insurance cover is about $3 per week. Young members can pay premiums just half this level but older members pay more, up to an average $3.70 per week.

The average amount of insurance cover varies from $150,000 for young super fund members aged under 20 years down to just $28,000 for super fund members aged in their sixties.

For members in higher risk occupations the premium price variations for 45 year old members range from a low of 87 cents per week all the way up $26.40 per week - for price range ratio of 30-times.

These findings are based on a study of 15,000 insurance deals on offer through 220 superannuation products conducted by Rainmaker Information, the researcher behind the SelectingSuper superannuation fund comparison and assessment service.

Stephen Fay, Rainmaker Information's head of superannuation research, said almost all super funds offer insurance to their members. But depending on the profile of the fund membership and the deal negotiated by each super fund with their insurer, members could be paying very different insurance premiums for the same level of cover.

"There is significant variation in the price of insurance super fund members pay. While the median premium amount for standard insurance cover paid by a 45 year old fund member working in a low risk occupation is $3.76 per week, the most expensive super fund charges $11.78. The cheapest funds charge as little as $0.48 per week which is a staggering 25-times less," said Fay.

Fay explained that the premium prices super fund members pay for their insurance is driven by their level of risk. For example, around 50% of super funds vary their insurance cover and premium prices according to the type of job or occupation in which the member is employed. Around 30% of funds vary their insurance cover based on the gender of each fund member.

"Super fund members in higher risk jobs will on average pay twice as much for their insurance cover as members in lower risk jobs," said Fay.

But even within these risk groupings there can be large price variations: "For a 25 year old super fund member with standard life insurance their cover could range from $50,000 to over $600,000 and their weekly premium costs could range from $0.45 to $7.80.

"However super funds providing the most insurance cover aren't always the most expensive." said Fay. "Members who don't compare their super fund's insurance premiums run the risk of paying hundreds of extra dollars each year in insurance charges for potentially the same level of cover."

Segment differences

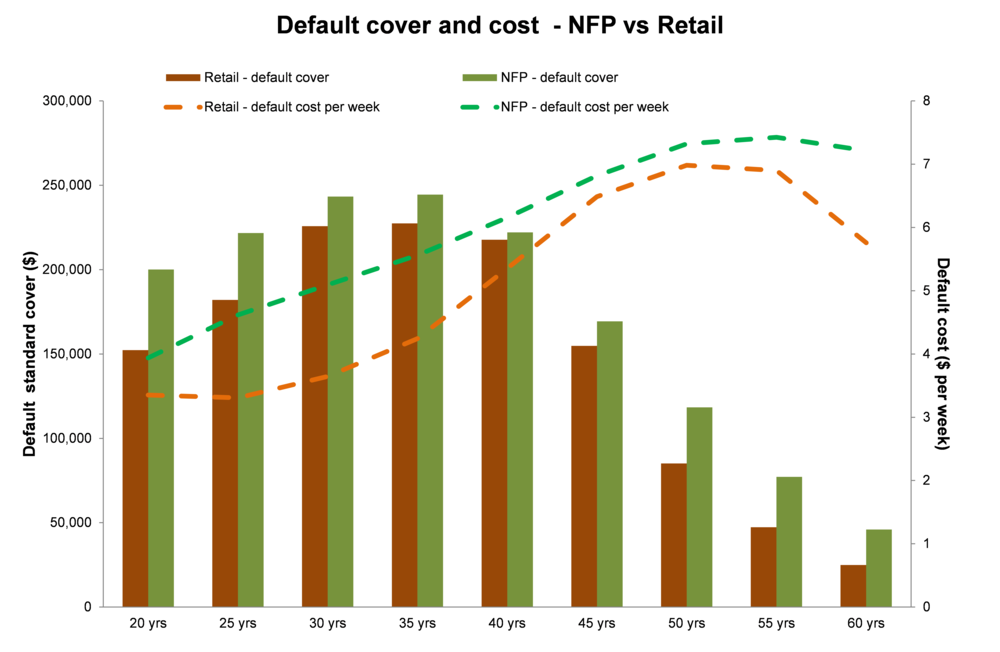

While Not for Profit (NFP) funds, i.e., corporate, public sector or industry funds, generally offer higher levels of standard cover default insurance than Retail funds, they normally provide this insurance cover at a cheaper rate. Consequently the average weekly cost of default cover is lower for NFP funds than Retail funds.

Rainmaker Information's research showed that standard insurance available for a typical 45 year old member in a NFP fund offers $169,300 cover which is 9% more than the $154,800 cover the same member would get in a Retail super fund.

The premium price our 45 year old member pays is however $6.82 per week in a NFP fund, which is only 5% more than the $6.49 per week they would pay in a Retail fund.

Changing insurance policy terms and conditions

As premium rates for insurance through superannuation have trended upwards in recent years, one important factor adopted to influence premium movement is super funds changing the terms and conditions that apply to these insurance policies.

For example, in concert with their insurers there has been a convergence on a tight policy condition that applies to Total and Permanent Disability insurance that is often bundled with death insurance. In the past, to claim on these policies many super fund members who had been severely injured or who have contracted a major illness would only have to prove that they can no longer perform their regular job. But in most current TPD policies, to successfully claim against these policies they will now have to prove they can no longer perform any job aligned to education and experience.

Furthermore some funds require far more involvement in rehabilitation process and continual disclosure.

Fay said: "While there is general consistency across many super funds' group insurance policies, there still exist some important differences that impact the member's ability to claim upon the policy. This is an important factor in addition to the price of the cover."

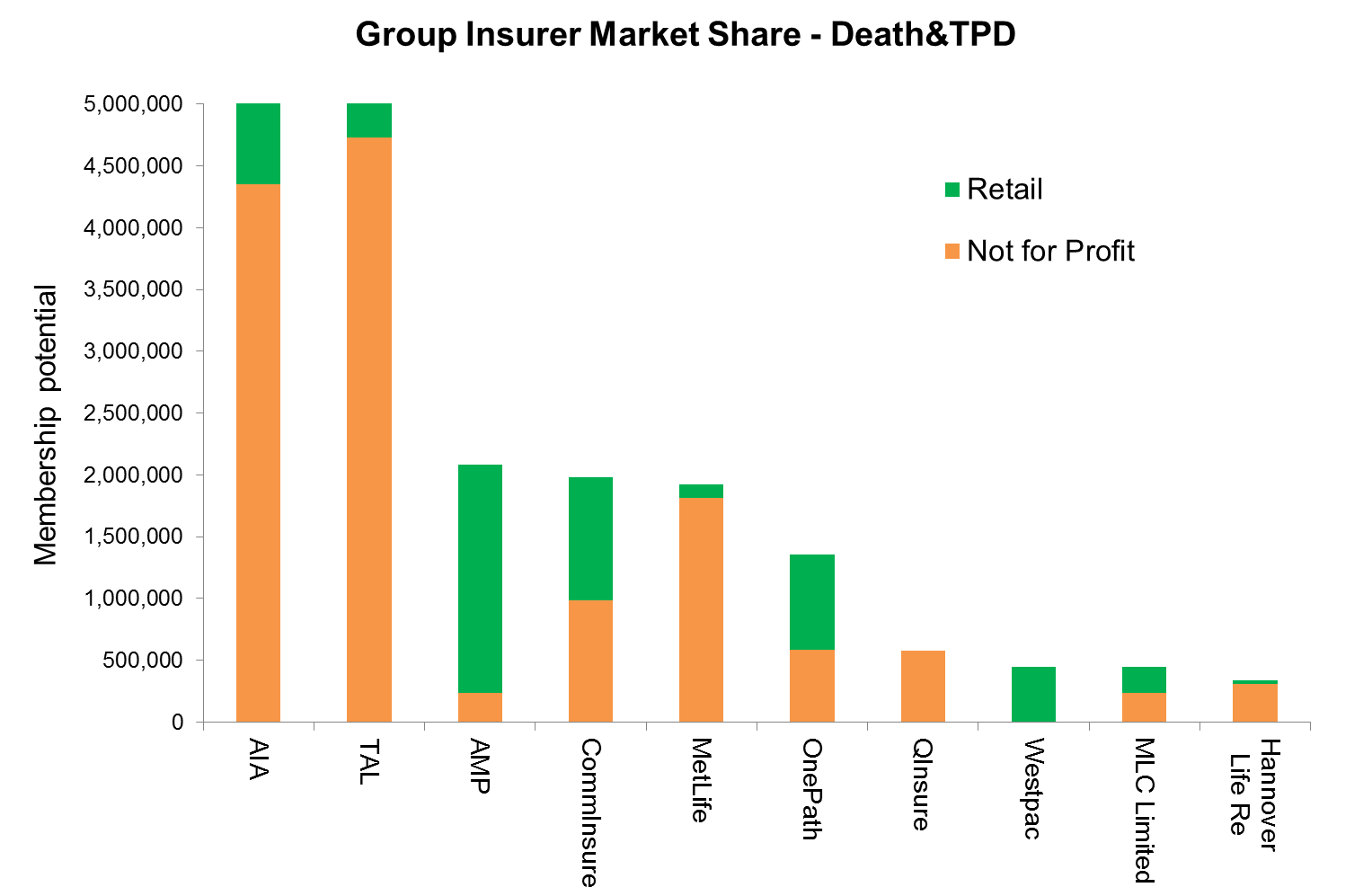

Insurer market share

The insurance companies partnering with super funds to provide insurance cover to the most fund members are AIA with 28% market share followed by TAL with 26%, and AMP, CommInsure and MetLife each with 10%. These 5 insurers control 84% of the market.

TAL has the largest market share for NFP fund members and AMP has the largest market share for Retail fund members.

Only one third of super fund members are covered by Australian owned insurers.

Super funds offering the best value and cheapest life insurance

The best value default life insurance for 40 year old members is offered by VISSF Accumulation, Australian Ethical Super, UniSuper, LGS Accumulation and Equip MyFuture.

The lowest cost standard cover life insurance for 40 year old members is offered by Triple S, UniSuper, Maritime Super, Media Super and Equip MyFuture.

But funds offering the high amount of insurance cover for 40 year old fund members are NGS Super Accumulation, legalsuper, smartMonday PRIME, REI Super and Australian Ethical Superannuation.

"Life insurance is an important core benefit offered by super funds where members can access cost effective wholesale prices. However with variation in overall cover provided, premium rates and weekly cost of cover, there is opportunity to choose an insurance that best fits. Some key comparisons has the potential to save members and their family thousands of dollars in annual insurance premiums," said Fay

The Tables and Charts over the following pages show which super funds offer the best default combined Death & TPD insurance deals for workplace superannuation products, variation in default cover between market segments, and insurer market penetration.

Super funds with the best insurance deals 2018

| Sum Insured ($ default level of cover) |

| |

|

|

|

|

|

| |

Product |

25 year old |

|

Product |

40 year old |

| 1 |

Christian Super |

669,600 |

1 |

NGS Super Accumulation |

450,000 |

| 2 |

legalsuper |

440,000 |

2 |

legalsuper |

440,000 |

| 3 |

smartMonday PRIME |

419,088 |

3 |

smartMonday PRIME |

419,088 |

| 4 |

LESF |

408,000 |

4 |

REI Super |

400,000 |

| 5 |

Lutheran Super |

403,200 |

5 |

AustEthical Emp |

398,502 |

| 6 |

CareSuper |

401,120 |

6 |

Rest Super |

386,000 |

| 7 |

VISSF Accumulation |

376,200 |

7 |

VISSF Accumulation |

376,200 |

| 8 |

LGS Accumulation |

345,000 |

8 |

QSuper Accumulation |

375,000 |

| 9 |

Child Care Super |

340,000 |

9 |

EISS Super |

332,000 |

| 10 |

QSuper Accumulation |

329,643 |

10 |

Kinetic Super |

329,400 |

| |

Sector average (median) |

200,000 |

|

Sector average (median) |

193,200 |

| Value (cover per $1 weekly premium) |

| |

|

|

|

|

|

| |

Product |

25 year old |

|

Product |

40 year old |

| 1 |

Kinetic Super |

234,118 |

1 |

VISSF Accumulation |

109,043 |

| 2 |

MyLife MySuper |

179,310 |

2 |

AustEthical Emp |

107,995 |

| 3 |

Catholic Super |

179,310 |

3 |

UniSuper |

97,619 |

| 4 |

Child Care Super |

139,344 |

4 |

LGS Accumulation |

87,099 |

| 5 |

UniSuper |

138,095 |

5 |

Equip MyFuture |

82,540 |

| 6 |

LGS Accumulation |

136,780 |

6 |

Triple S |

80,000 |

| 7 |

Rest Super |

135,417 |

7 |

Virgin Super Employer |

78,605 |

| 8 |

QSuper Accumulation |

134,001 |

8 |

LESF |

73,585 |

| 9 |

NGS Super Accumulation |

125,000 |

9 |

ACSRF Employer |

71,705 |

| 10 |

Equip MyFuture |

120,930 |

10 |

MyLife MySuper |

68,421 |

| |

Sector average (median) |

53,561 |

|

Sector average (median) |

41,817 |

| Cost (weekly $ cost to member) |

| |

|

|

|

|

|

| |

Product |

25 year old |

|

Product |

40 year old |

| 1 |

Rest Super |

0.48 |

1 |

Triple S |

1.50 |

| 2 |

NGS Super Accumulation |

0.96 |

2 |

UniSuper |

1.68 |

| 3 |

Kinetic Super |

1.02 |

3 |

Maritime Super |

2.00 |

| 4 |

MyLife MySuper |

1.12 |

4 |

Media Super |

2.20 |

| 5 |

Catholic Super |

1.12 |

5 |

Equip MyFuture |

2.42 |

| 6 |

Energy Super |

1.14 |

6 |

LUCRF Super |

2.55 |

| 7 |

Club Plus Industry |

1.20 |

7 |

Club Plus Industry |

2.76 |

| 8 |

Essential SE |

1.30 |

8 |

Catholic Super |

2.77 |

| 9 |

Triple S |

1.50 |

9 |

MyLife MySuper |

2.77 |

| 10 |

WA Super |

1.65 |

10 |

IOOF ESE |

3.00 |

| |

Sector average (median) |

3.18 |

|

Sector average (median) |

5.44 |

Source: Rainmaker Information - www.selectingsuper.com.au

![Default superannuation insurance cover and cost]()

![Default superannuation insurance cover and cost]()