![understanding superannuation fees and if you]()

To understand how much you are really paying in superannuation fees, you have to demystify the different ways products and funds describe them.

- The more fees you pay, the higher your investment returns must be to make up for them.

- While there are many types of fees, you can group them together to derive your overall total expense ratio.

- Fees are now capped at 3% if your account balance is less than $6000, while exit fees are now banned.

Your aim in selecting a MySuper product or superannuation fund is to find one that will make you as financially independent as possible by the time you retire or leave the workforce, without exposing you to too much unnecessary investment risk along the way.

To do this, your super fund must earn consistently strong rates of investment returns net of fees - year in, year out. Fees affect your investment returns

To give you a better chance of building your retirement savings, it helps if your MySuper product or super fund charges only low or reasonable fees.

Why? Because what you get in your pocket is what's left from the investment returns after all the fees are taken out - it is as simple as that. So the higher the fees, the higher the returns have to be to leave you with more money in your pocket.

An example will highlight why this is so important to understand.

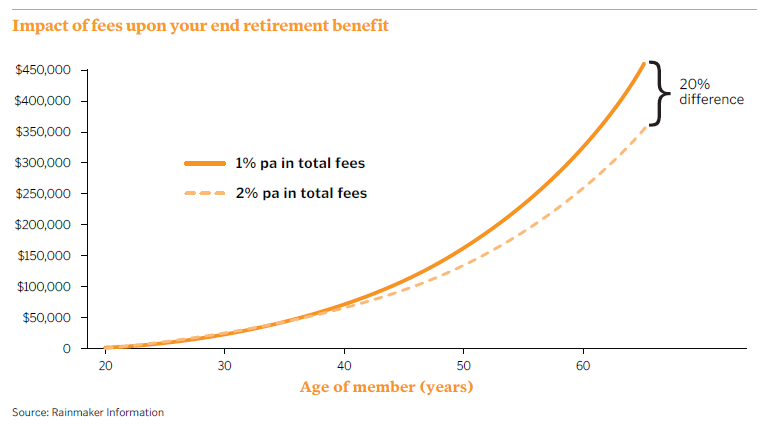

If two 20-year-old super fund members achieve identical investment returns but one pays only 1% in fees each year while the other pays 2% in fees each year, the member in the higher-fee fund will retire with 20% less. This impact is shown in the graphs later in this chapter. So paying higher fees can cost you big money.

And this means that if you are paying higher fees you should make sure you use the fund shrewdly, so that you more than make up for these fees through better investment mixes and higher returns.

All about the fees

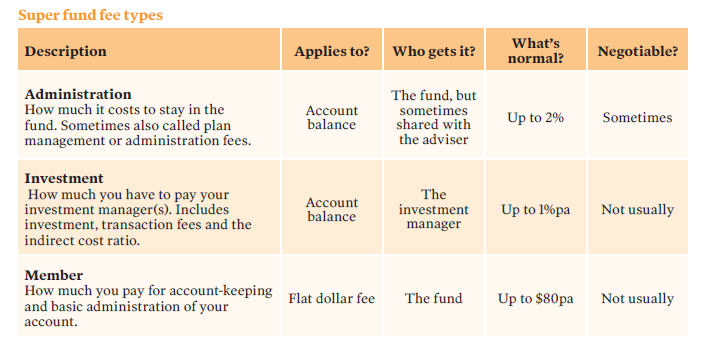

When checking out superannuation fees, there are three main types you should know about, as shown in detail in the table at the end of this article. These are:

• Administration fees are percentage-based fees paid to your superannuation fund to cover its regulatory, administration, platform, compliance, technology and marketing costs. • Investment fees are paid to your fund's investment managers and asset consultants. These fees might also be called transaction fees, the new name for the indirect cost ratio, which is also charged as a percentage of your account balance.

• Member fees are dollar-based fees paid to your super fund, usually to cover account keeping. Some funds used to also charge contribution fees, also known as entry fees, that were paid to financial advisers when you join the fund. But because advisers can no longer receive commissions from superannuation products, these fees are rarely charged nowadays.

These fee types mean that the different people involved with your super are getting a different share of your fees.

For example, in many super funds, the investment managers may be receiving two-thirds of the fees you are paying.

Some funds may also bundle their management and investment fees into a larger combined figure, meaning that if your fund reports a zero investment fee, it doesn't mean it is investing your superannuation for free; it simply means it has structured its arrangements differently.

You can often get discounts on this fee if you ask for it or if you are contributing a large amount of money into your superannuation fund. When working out your total fees, don't forget to also count the member fee.

If you are starting out in super, this member fee is your biggest headache, and funds that might at first seem expensive can sometimes be cheaper for you because they don't charge a member fee. For example, if you have only $1000 in your fund, a $1.50 per week member fee is costing you $78 per year.

This converts to 7.8% of your account, which is likely to be five times the combined management and investment fees.

Of course, these ratios change quickly as your account balance grows.

There are also some tricks of the trade you should watch for when it comes to fees and charges. For example, some products or funds claim to have low or even zero fees, even though they make this happen by deducting extra costs from their earnings rates before declaring your crediting rate.

Watch out especially for funds that try to confuse you by talking about fees charged to the fund and how they are different to fees charged directly to you.

Anything that comes off the top of your return before you receive it is a fee to you - no ifs, no buts.

![good super guide impact of fees on retirement]()

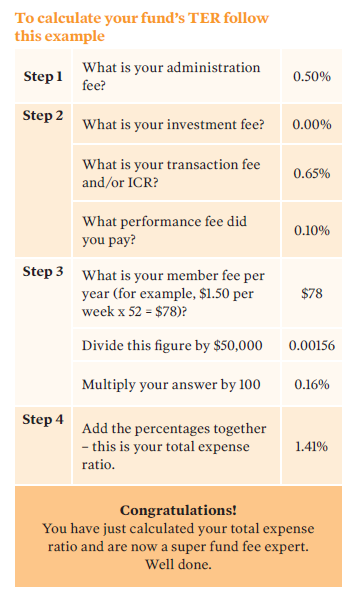

Calculating your super fees

A fee calculation converts all the fees you are paying into a single dollar amount. It then applies that amount to your overall account balance to come up with your total fee as a percentage of your account balance. We call this percentage your total expense ratio, or TER.

Knowing the different fees charged by different products and super funds means you can calculate the different TERs.

It is important to realise, however, that a TER does not indicate the future performance of a fund - but we do know that higher fees rarely lead to better investment returns. Proving this, many of Australia's top-performing MySuper products and super funds usually have low fees anyway, so why pay higher fees if you don't have to?

For most members with $50,000 or more in super, the biggest fee culprit is the administration fee because it is usually the highest, while the fee with least impact is the member fee (once your account balance grows) because the $1.50 per week converts to only 0.16% on a $50,000 account balance.

The member fee, however, has a bigger impact when you're starting out in superannuation and you have a smaller account balance. As a result of this, if you want to receive a deal on your super fund fees, you will get the best results if you dial down the management fees. It is, of course, good if you can dial down other fees, but it's the management fees that you should worry about first.

![good super guide calculate ter]()

While the average superannuation member across Australia pays a TER of about 0.95%, this covers everybody whether they are in SMSFs, public sector schemes, not-for-profit and retail funds.

A better comparison is that if you are in an industry or retail fund and paying less than 1%, you are in a very sharply priced fund, while if you are paying between 1% and 1.2% you are paying a reasonable price, but anything above 1.2% is expensive.

New laws passed in 2019 banned super funds from charging fees above 3% if you have less than $6000 in your super fund account and also banned exit fees.

To comply with this new 3% fee cap, super funds aren't necessarily lowering their fees but at the end of each year if you have less than $6000 in your account they will refund any fees you have paid above the 3% threshold.

Some workplace retail funds, such as corporate master trusts, meanwhile, can sharpen their fee deals for some client companies to such an extent that there may be hardly any difference between their fees and those of a low-cost industry fund.

This is because most corporate master trusts will negotiate on fees, and if you represent a company or you have a sizeable amount of superannuation in your company account you should never be afraid to bargain hard for a better deal.

Reflecting this, simple comparisons of the fee rates don't always tell the whole story.

![good super guide super fund fee types]()