Most super funds have been designed for older people with high account balances, so how can you find a good super fund for young people who are just starting out?

When you're starting out in superannuation, fees matter more than performance.

Look for percentage fees that are less than 1%pa.

Watch out for funds that charge dollar-based membership fees.

Insurance will cost you more than your regular fees. If you're young and don't need it, think hard before agreeing to buy it.

When you're young and just starting your working life, superannuation and your future retirement will probably be the last thing on your mind. You won't be too worried about your choice of super fund and you'll be quite happy to join the one you're told to join or one with a high profile brand that you like.

If you're lucky, this can be a good strategy - you'll join a good-value, strongly performing super fund that offers great product features. But not everyone is so lucky. To ensure you get off to a good start in your superannuation life, there's a few things to know:

Superannuation is compulsory for most people, and it's your money; and

A super fund is just a savings account purpose-built to help you save for your retirement.

Fees matter more to young people

Super funds charge fees that are a combination of percentage-based investment and administration fees charged against your account balance and a flat dollar-based member fee.

In 2025, default MySuper products charged an average fee of 0.93%, made up of 0.19%pa for administration, 0.65%pa for investment management and $62.40pa for member fees. Administration and member fees counted together are also called product fees.

But when Rainmaker Information and people in the superannuation industry talk about fees, they usually mean the fees that apply to people with $50,000 in their account. When you're young and starting out, you won't have $50,000, but probably only a few hundred or maybe a thousand dollars.

If this is you, you could be paying fees of 10% or more. Even though fees above 3% will now be refunded to you at the end of each year, this means that the money you've paid in these high fees wasn't being invested for you. In any case, why pay high fees if you don't have to?

Because of this, young people often pay fees that are about eight times more than the 1.1% average paid by older people.

Insurance and the total cost of super

Members who are under age 25 don't have to buy compulsory life insurance through their super fund.

Once you are 25 and over, if you are a member of a MySuper product, you do have to, even though you can choose to opt out (cancel it) at any time. This life insurance can be a mix of death insurance, total and permanent disability insurance and income

protection insurance.

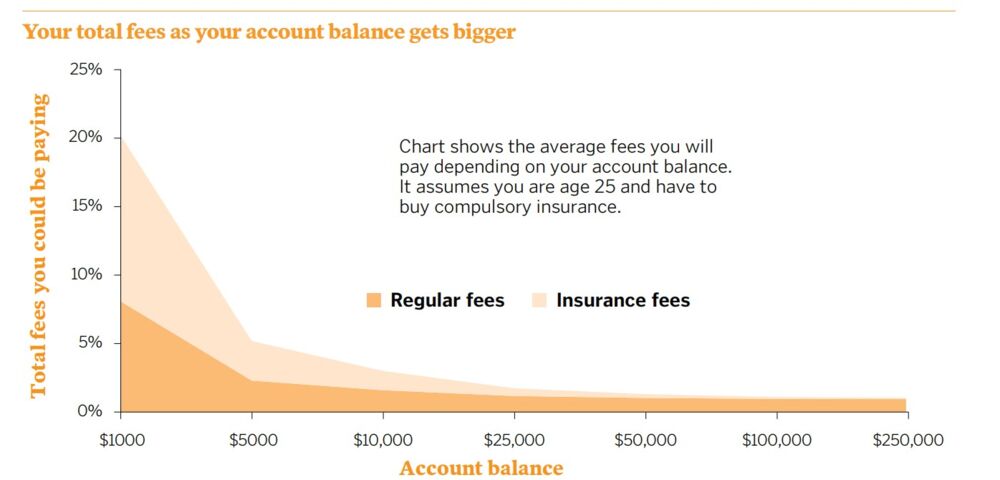

While this insurance is cheap in overall terms, averaging $139pa for $169,000 cover if you are 25 years old, if you have $5000 in your super account it converts to 3.2% of your account balance. Adding this insurance fee to the regular fees means that you are now paying 6%pa in total fees.

But the scary part is that if you are just starting out and have only about $1000 in superannuation, you could be paying total regular fees and insurance fees equivalent to 25% of your account balance. The chart shows you how this works.

The point we are trying to highlight to young people is that while Australia has a lot of very good super funds that will earn you good investment returns and provide you with great deals on insurance, most of these funds have been designed for older people who have more money in their accounts.

Young people need to look at their superannuation a bit differently.

Features all good super funds should have

Every smart, modern super fund should have a good website with lots of useful, easy-to-understand information, online account access, be easy to deal with and most likely have a smartphone app.

But this doesn't matter much if you don't trust the fund, if its performance isn't any good and it's expensive.

Aware Super acquires $226m real estate investment22 July 2026, 12:15pmAware Real Estate has expanded its Sydney CBD office portfolio, acquiring a 50% stake in 100 Market Street for approximately $226 million in a move that strengthens its exposure to prime commercial real ... Read more

Fight between SMC and FSC on super rages on22 July 2026, 12:06pmThe Super Members Council (SMC) has called out the Financial Services Council (FSC) on making selective claims about performance and costs of 'platform' super funds compared with performance-tested mainstream ... Read more

UniSuper backs tech despite AI caution17 July 2026, 12:13pmUniSuper has reaffirmed its conviction in the global technology sector after delivering another year of double-digit returns in its Balanced option. Read more

AusFood Super looks to revitalise member engagement15 July 2026, 11:30amThe $3.5 billion super fund has partnered with InvestStream to launch RetireSmart+, becoming the first super fund to bring an AI-powered engagement experience to some 66,000 members. Read more

When comparing super funds and considering what is right for you, look for funds displaying the AAA Quality Assessment and Rainmaker SelectingSuper Award logos.